The Cassandra Economist

Economists Have Not Been Made Omnipotent: We Have Limits

Last week, my friend Marco Annunziata gave thanks for being an economist with his usual wit. I won’t spoil his great piece, which I strongly recommend.

I am an economist as well, and, as Marco knows, I agree with everything he says in his post. What I would add in our defense is that everyone is fallible, and hence any profession has strengths and weaknesses. The problem with economists is that they mostly seem unaware of those weaknesses or are strongly determined to ignore them.

When, during a dinner conversation, you happen to be sitting next to an economist (note how, by choosing the phrase "you happen," I try to remain positive about what Fate had in mind for you), most of the time you’re in for an amusing evening, even when the economist next to you doesn’t intend to be amusing. Whatever topic you introduce, when the time comes for them to speak (we are quite polite, you see?), most of the time we will begin with some act of modesty—something like, “I can only speak as an economist” or “from the limited perspective of an economist.” But immediately after, we will gingerly breach our self-imposed limitation and speak about anything with authority and conviction, as if we were infallible experts on the matter. So, you see, it can be very entertaining—if you don’t take us too seriously.

Let me try to share my thoughts on the roots of this behavior.

As I mentioned, I am an economist, and I am grateful I turned out to be one and for everything studying and practicing economics has taught me. I think the best gift economics offers is structured thinking. This is unfortunately such a rare ability nowadays (at least, judging by what people privately and publicly share). ChatGPT, an excellent example of structured thinking, defines it as "the ability to organize and process information logically, systematically, and clearly. It involves breaking down complex ideas into smaller, more manageable components and arranging them in a coherent framework that facilitates understanding." I love this definition because it stops at ‘understanding.’ Structured thinking is best at understanding.

This is no small feat. Understanding things that happen in our complex world is an extremely valuable currency (valuable because rare—another concept economists learn at the beginning of their studies). The problem is that, endowed with such a priceless ability, we get immediately greedy and venture into the successive steps: explanation and action. This is where the sand gets into the gears, because explaining and acting require a totally different set of skills: communication, decision-making, and the skill that economists are almost naturally lacking—compromise.

Compromise is difficult. It is a complex mix of belief in your ideas and the ability to listen to others’ ideas and find common ground, close enough for both parties to gladly bend toward. This is so difficult for economists because the ‘understanding’ part is so strong that we always start with the idea that we have a much better grasp of the matter at hand than our counterpart, even when they are also economists. Where else have you seen a self-proclaimed science coexisting with so many antagonistic theories about inflation, money, value, price, and so on?

I have learned this lesson the hard way, through some monumental mistakes I made when I tried to go beyond ‘understanding.’ In Italian, we have a saying: "far danni." It loosely translates to "do harm," but in English, it lacks the nuance of childishness that the Italian version fully implies.

It is no wonder that my favorite economic theory is that of ‘optimal choice.’ It is such an elegant framework to understand how economic agents (individuals, households, corporations, governments) make decisions to maximize their satisfaction (utility) or profit, subject to certain constraints like income, prices, or available resources. I have always been extremely fascinated by it, and I consider it one of the pinnacles of economic theory.

The theory of optimal choice is so clear, so convincing when interpreting human behavior, and yet it remains modest and very abstract. It understands but stops short of explaining and—especially so—acting.

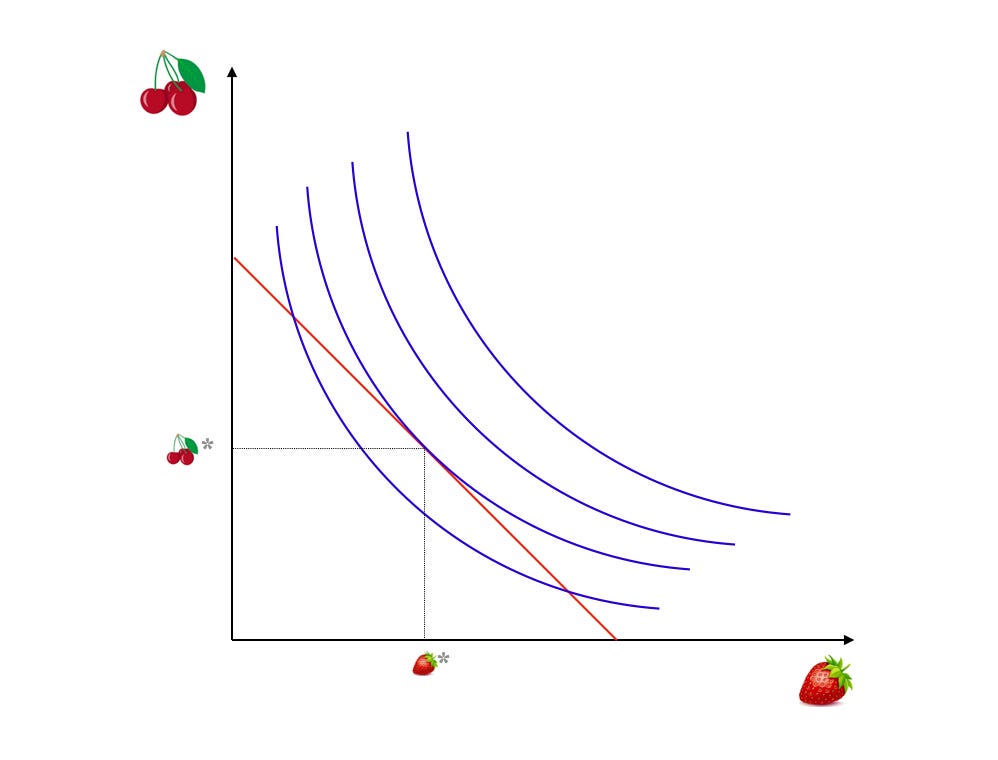

Imagine me, a hungry consumer passing in front of a fruit shop that only sells cherries and strawberries. What should I buy to be happy? The two axes represent the amount of cherries and strawberries I could purchase. The red line is the so-called ‘budget constraint.’ I pat my pockets and find out that I have X dollars. Of that X, I want to spend Y (because I want to save money). So, the red line on the graph represents the combinations of cherries and strawberries I can buy by spending Y (for example, 300g of cherries and 200g of strawberries, or 150g of cherries and 350g of strawberries). The higher Y is, the farther to the right the red line shifts, because I can buy more of both fruits by spending more. The slope of the red line reflects the (relative) price of cherries and strawberries. We don’t need to dwell on this.

If the red line represents all the combinations I can afford, which one would I choose to be happiest? Enter the genius of economists like Edgeworth, Pareto, Fisher, and Hicks, the latter on his sublime treaty ‘Value and Capital’. The blue curves are ‘indifference curves,’ which describe combinations of cherries and strawberries that would produce the same satisfaction (or ‘utility’) for me. Indifference curves farther to the right indicate greater happiness (though they didn’t factor in the consequences of consuming infinite cherries, such as diarrhea).

The model thus understands consumer choice as the interaction of budget constraints (income and prices) and preferences (indifference curves). Geometrically, the optimal choice is the point where the budget line tangentially touches an indifference curve. OMG, SO ELEGANT!

The theory understands. It DOES NOT explain (what is an indifference curve, anyway?). It certainly does not act on it(self): we should be grateful it does not because it assumes rational behavior (a huge mistake in today’s world) and ignores external factors.

Understand, don’t explain, and certainly don’t act.

This feels like a curse for us poor economists: Cassandra’s curse. She was the daughter of King Priam and Queen Hecuba of Troy. According to the myth, Apollo fell in love with her and granted her the gift of foresight. When she rejected him, he cursed her so that her predictions would always be true, but no one would believe her. Economists should learn from her frustration: understand but don’t persuade.

I have one wish for us economists. We need to be grateful for and embrace our (superhuman) gift of understanding, thanks to structured thinking. But that understanding will be wasted if we don’t trust others—communicators and mediators—to bring forward our ideas and make the best of them for humanity.

Be modest. Non fare danni!

lol the subtle cue on how no one would choose to sit next to an economist

lol i can think of quite a few other species that's unaware of their limitation, hollywood, elon, trump...

Luca, this is a delightful and laudable effort to partially redeem our species in the eyes of the general public. I wonder if one can argue that economists often suffer from a 'reverse Cassandra curse': to be believed in the many cases where our predictions are actually badly wrong....

As I reflect on your article, I am now tempted to argue that economists should in fact try harder to explain their views. I do see the significant risk of 'far danni', but I wonder if trying to explain can help them / us realize when in fact we do not understand things nearly as well as we think we do.

In any event I do find the Cassandra comparison quite appropriate -- all the more so for a Substack dedicated to the End of Times :)