"Someone's gotta do it."

Must they, really?

I eagerly await Saturdays — and not (just) because it’s the weekend.

More importantly, it’s the day my friend Marco Annunziata publishes his weekly blog on Substack. I usually leave a comment, less because I have something brilliant to add, and more to affirm how deeply I agree with him — and to say, once again, that he’s one of the few intellectually honest economists out there.

But today is different.

Today, I disagree so fiercely with one of his statements that a simple comment won’t do. It deserves a longer response.

One sentence, in particular, leapt off the page and poked me right in the eye — perhaps because I found myself nodding so vigorously with everything else around it.

“Forecasting the economy is a dirty job, but someone’s gotta do it.”

And I couldn’t help but think: Really? Must they?

Let’s play a game. List institutions that might need the 2025 global economic forecast and ask ourselves: Do they really need it?

Governments, in theory, just might; to plan budgets and set fiscal policies. In theory.

But can you actually picture elected officials eagerly waiting by the screen for the IMF or World Bank to update their global forecast before announcing the next budget?

I can't.

Having lost ideologies, modern politics has become so intensely partisan that budgets and policies are often set more by "mood" than by macroeconomic projections. When growth forecasts are revised upward, the ruling majority throws a party and quotes independent forecasters like gospel. When forecasts are downgraded, Prime Ministers suddenly discover their allergy to "experts," while the opposition starts handing out copies of the report like campaign flyers.

I have hardly seen policy and budget plans withdrawn after the IMF amended the economic growth forecast by 0.4%—unless they would have done so anyway. If a politician tells voters that their decisions depend on what the IMF has to say, I am not very optimistic about their future career: voter sentiment, on often much more mundane matters, moves politicians’ hearts; not the IMF’s decimal points.

Then there are businesses, as in non-financial corporations. In theory, they would treat global economic forecasts as the bedrock for strategic decisions: how much to produce, where to source components, which market to bet on next.

And yes, it's probably true that a corporation armed with a flawless crystal ball would perform (marginally) better than its competitors — assuming, of course, they actually understand what a shift in GDP forecasts really means for their own business.

Except that if business decisions truly rested on serious, rigorous assessments of future economic activity, then every serious, rigorous company would be packed with brilliant economists. But that’s far from reality. Chief Economists are a rare breed in non-financial corporations — and when they are found, they're often wheeled out to say a few polite words at board meetings, or worse, to sit through a ‘guest star economist’ delivering a thirty-minute keynote at the annual company retreat.

A partial excuse for businesses’ cheerful indifference to economic forecasts is that in today’s hyper-competitive, short-cycle corporate world, basing decisions on the same data everyone else uses won’t give you an edge. Besides, the kinds of serious, strategic decisions where managers might actually need a reliable forecast typically unfold over timeframes far longer than the neat two- or three-year horizons favoured by the IMF or World Bank.

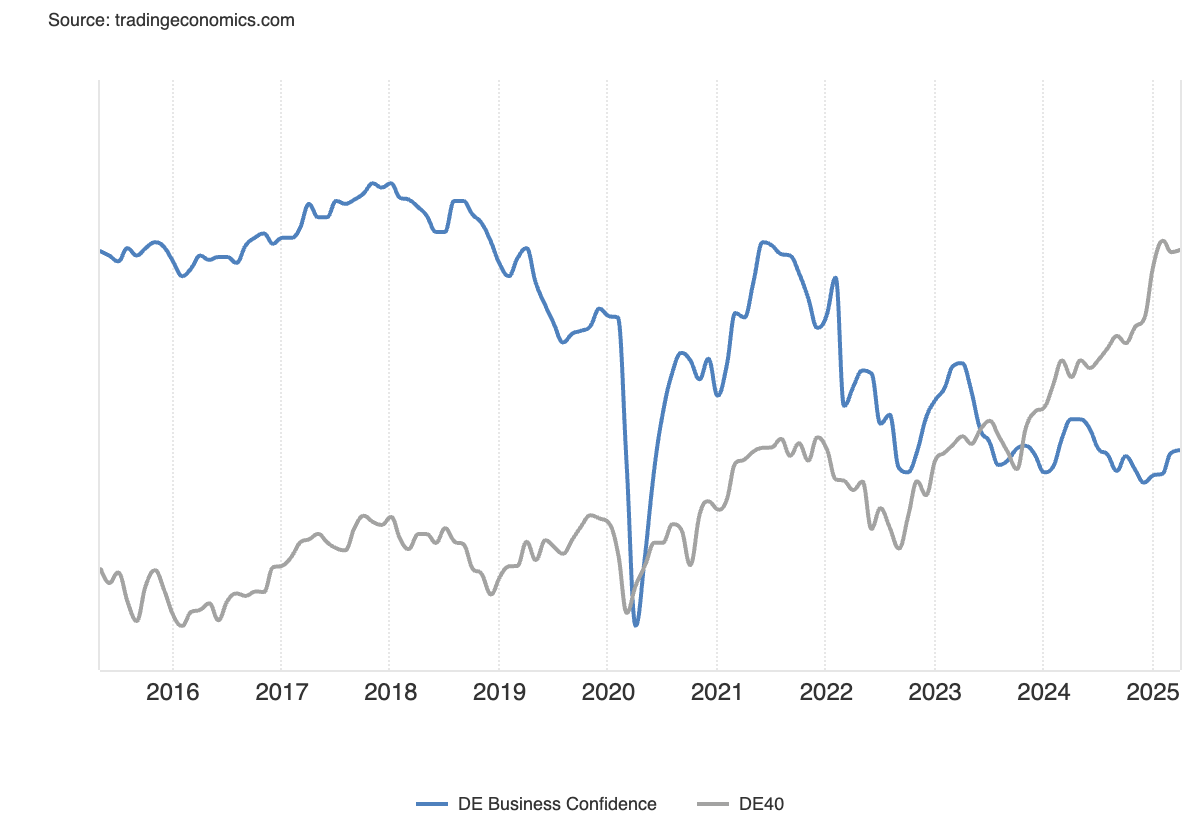

But what about investors? Surely they must rely on economic forecasts to make the right decisions, right? Think again. Take a quick glance at the chart below: over the past three years, Germany’s DAX 40 — the country’s main stock market index — has shattered record after record, defying gravity and the most grim business confidence outlook ever recorded in the series.

I suspect investors are far too busy chasing hype, herding into bubbles, and panic-selling the next day to sit quietly and read a 200-page growth outlook. With daily gyrations the size of developed countries’ GDP, the matter has become too serious to be based on economic forecasts. Deep-pocketed market participants have probably learned long ago that real money is made not by forecasting the economy, but by forecasting everyone else's mistakes – including Central Banks’.

Well, wait a moment. Did I say Central Banks? Well, they, at least, must need global economic forecasts as direct or indirect factors behind their policy rate decisions. Perhaps, but most of them have their own fully staffed economic forecast departments, which couldn’t care less about what the IMF says. If anything, global forecasts are politely skimmed for diplomatic reasons, then tossed onto the growing pile of ‘external inputs’.

Judging by some recent central bank actions, monetary policy today seems to depend very little on economic data. It’s more about printing money when markets need it (always) and creating imaginative narratives and ‘forward guidance’ that the market plays with for a while—long enough to make central bankers feel important—before shelving it and getting back to serious business.

Who else? Is there really nobody who really thrives on global economic forecasts nowadays?

Oh, yes, silly me. The media loves a good downgrade to splash on the front page, even if these days, given the far juicier news cycle, it typically lands somewhere around page three or four.

But is that enough? Enough to justify legions of economists (myself included) furiously mining the hidden depths of their brains and models to produce a single, fragile number?

Let me end on a less sarcastic note.

As Marco, I have genuine respect and sympathy for my colleagues who are tasked with the impossible job of forecasting something real — the future of the economy — using purely quantitative and entirely theoretical econometric models. But I believe that these grand exercises by reputable institutions once carried greater meaning, even when they turned out to be wrong, in the more opaque world of the past, when information was scarce and costly.

One could argue that today, bombarded every second with overwhelming torrents of competing information, there is an even greater need for voices that make a conscious effort to filter the noise and present ‘the truth’. And yet, when I look at these exercises, I struggle to see what, exactly, qualifies them for that role.

I should also have noted: normally I read your blogs as soon as they hit my mailbox, but this time as you published it I was hard at work preparing lunch, we had a couple of friends over to discuss economic forecasts over steaks and wine...

Your excellent post leaves me in the rather odd and awkward position of finding myself unable to disagree with someone who disagrees with me.

I was about to take issue with the kind words you spent on me, but then i noticed with great relief that they are part of the sarcastic section of your blog, so even on that front all is in order.

I will just underscore your last point -- I could not agree more.